Foreign nationals can buy a house in Japan with the same legal rights as Japanese citizens, no visa, residency, or citizenship is required. The process takes about 60 to 90 days, total purchase costs typically run 5 to 6 percent of the price (plus 1 to 2 percent for mortgage buyers), and from April 2026 non-residents must file a Bank of Japan FEFTA report within 20 days of acquisition. Housing Japan is licensed by Tokyo Metropolitan Government and has guided expat buyers through this process for 25 years.

Key Facts for 2026

- There are no nationality restrictions on buying property in Japan.

- Total buying costs typically run 5–6% of the purchase price, plus 1–2% in bank fees if you use a mortgage.

- The brokerage fee is capped at 3% + ¥60,000 + 10% consumption tax.

- From April 2026, non-residents must file FEFTA Form 22 with the Bank of Japan within 20 days of acquisition.

- From April 2026, all buyers must disclose their nationality at registration, this is a disclosure rule, not a restriction.

- A typical purchase, from offer to keys, takes 60–90 days.

Can a Foreigner Buy a House in Japan?

Yes. A foreigner can buy a house in Japan with the same legal rights as a Japanese citizen. You do not need to be a resident, hold a visa, or have lived in Japan before. The Real Property Registration Act applies the same rules to every buyer regardless of nationality, and there is no quota on how many units in a building can be foreign-owned.

This makes Japan one of the most open property markets in Asia. The legal right to buy is completely separate from the right to live in Japan, so many international buyers complete their purchase while visiting on the standard 90-day visa-free entry available to nationals of the United States, the United Kingdom, Australia, and 71 other countries (Ministry of Foreign Affairs of Japan). Owning a property does not grant residency; to live in your home long-term, you still need a separate work, spouse, or business visa.

The practical work, finding a property, financing, contracts, and registration, is more involved than the legal question. The rest of this guide explains exactly how the process works, what it costs, and what changed in 2026.

How Do You Buy a House in Japan? Step-by-Step Process

Buying a home in Japan typically takes 60 to 90 days from your first offer to receiving the keys. The process follows eight defined steps. Knowing them in advance helps you plan your travel, your finances, and your paperwork.

1. Choose an Experienced Bilingual Agent

In Japan, your real estate agent does work that in many other countries belongs to a lawyer. Licensed brokers handle market research, negotiations, contract drafting, and the legal paperwork around title transfer. A bilingual, licensed agent is your single most important professional. The right agent provides:

- Legal safety throughout the transaction

- Translation and clear explanation of Japanese-language documents

- Advisory on pricing and current market trends

- Property viewing coordination and on-site due diligence

- Guidance on market standards and realistic expectations

- Negotiations and formal contract handling with the seller

Tell your agent your target area, property type, budget, and timeline at the first meeting. A good agent should also screen for off-market listings, which make up a meaningful share of central Tokyo luxury inventory.

It is important to work with a licensed real estate agent based in Japan. Under the Real Estate Transaction Business Act, only brokers licensed by a prefectural governor or MLIT can legally handle property transactions, and every agency must have a qualified Real Estate Transaction Specialist (宅建士, takken-shi) on staff to deliver the Explanation of Important Matters before signing. A Japan-based licensed agent also gives you access to REINS, the national listings database, plus local knowledge of building condition, zoning, and pricing, none of which an overseas-only or unlicensed introducer can legally provide.

2. View Properties On-site

3. Talk to a Bank About Financing

If you are paying cash, you can skip this step. If you need a mortgage, start the conversation with a bank before you make an offer. Japanese banks can provide an informal pre-approval that strengthens your position when you make an offer. Resident buyers with stable Japan income have access to standard rates from major banks. Non-resident buyers have fewer options, and most lenders will require a much larger deposit. Some specialist banks do work with non-residents but usually come with higher interest, large downpayments and capped borrowing amounts.

4. Submit a Letter of Intent

Once you decide on a property, your agent submits a Letter of Intent (買付証明書, kaitsuke shōmeisho) to the seller. This expresses serious purchase intent and sets out your offer price and conditions. Letters of Intent are usually treated on a first-come, first-served basis, so having financing already lined up gives you a real advantage.

5. Negotiate Terms and Sign the Purchase Contract

Your agent negotiates price, payment timing, fixtures, and handover conditions with the seller’s side. This usually takes one to two weeks. When terms are agreed, both parties sign the formal purchase contract. At this stage, a cash deposit (手付金, tetsukekin) of 5–10% of the purchase price is typically paid directly to the seller. This often surprises foreign buyers, since earnest money in many other countries is held by a third party such as an escrow agent. The idea behind the practice is that Japan is a trust-based society, paying part of the cost up front is a sign of commitment and solidifies trust between buyer and seller. Even buyers using a mortgage need to bring this deposit in cash.

6. Review the Explanation of Important Matters

Before signing, your agent provides the “Explanation of Important Matters Regarding the Property and Transaction” (重要事項説明書, jūyō jikō setsumeisho). This document covers ownership type, building condition, management association rules, zoning, and cancellation provisions. Reputable agencies provide an English translation, but only the Japanese version has legal effect, translations exist solely as reference. This is why bilingual representation matters.

7. Final Loan Approval (Mortgage Buyers Only)

If you are using a mortgage, your final loan approval comes through after the contract is signed. You will sign the loan agreement at the bank, usually on a weekday and lasting several hours. Cash buyers can move directly to settlement.

8. Final Settlement and Title Transfer

Settlement usually happens at the buyer’s bank and is handled by a judicial scrivener (司法書士, shihō shoshi). The buyer transfers the remaining balance to the seller’s account, the keys are handed over, and the scrivener files the ownership transfer at the Legal Affairs Bureau. Your name appears in the official property register within a few business days, which is the moment you become the legal owner, not the contract signing.

Let the professionals take care of every step of the process, Contact our Expert Bilingual Tokyo Real Estate Agents with over 25 years of eyepiece for more information.

How Much Does it Cost to Buy a House in Japan?

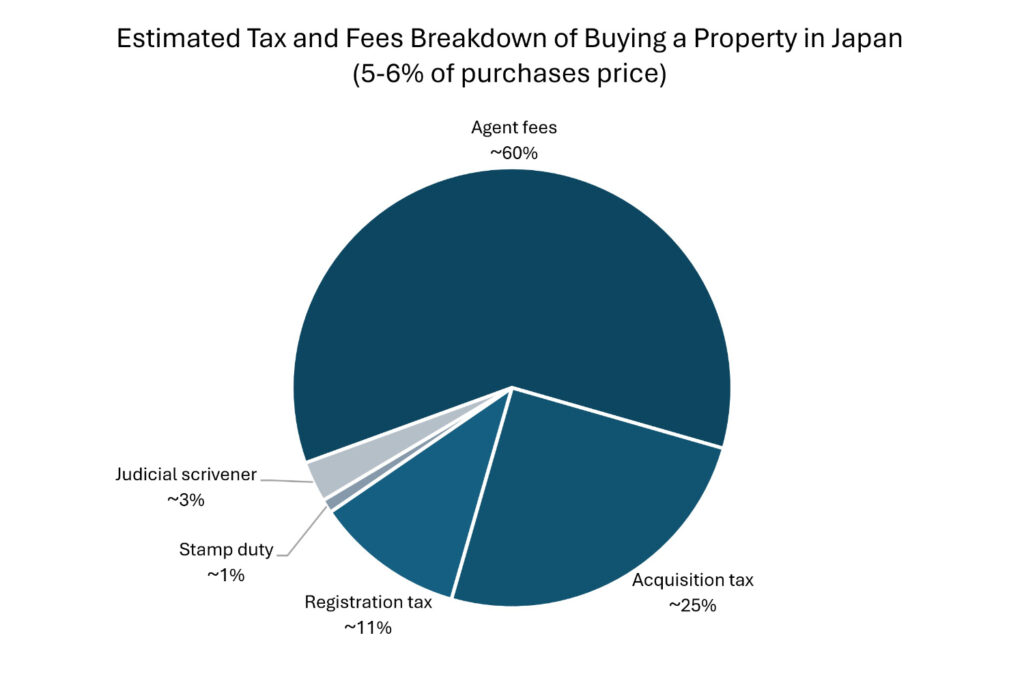

Total purchase costs in Japan typically run 5 to 6 percent of the purchase price. If you use a mortgage, expect an additional 1 to 2 percent in bank-related fees on top of that. The breakdown below uses official rates from the National Tax Agency, the Ministry of Land, Infrastructure, Transport and Tourism (MLIT), and Tokyo Metropolitan Government for 2026.

| Cost | What it is | Typical rate (2026) |

| Brokerage fee | Paid to your real estate agent on a successful purchase. Capped by MLIT. | 3% of price for buyer + ¥60,000 + 10% consumption tax (≈3.3%) |

| Registration & license tax (land) | Paid to register the land transfer at the Legal Affairs Bureau. | 1.5% of assessed value (reduced rate extended to 31 March 2029); standard rate 2.0% |

| Registration & license tax (building) | Paid when ownership of the building is transferred or first registered. | 2.0% standard; 0.1%–0.3% reduced for qualifying homes (until 31 March 2027) |

| Real estate acquisition tax | One-off prefectural tax billed 3–6 months after registration. | 3% on residential land and homes; 4% on non-residential buildings (3% rate runs until 31 March 2027) |

| Stamp duty | Revenue stamp affixed to the purchase contract. | ¥10,000–¥60,000 for most homes (¥100m–¥500m: ¥100,000) |

| Judicial scrivener fee | Pays the legal professional who handles the title transfer. | ¥80,000–¥200,000 (more for mortgages) |

| Annual fixed asset tax | Paid every year by the registered owner as of 1 January. | 1.4% of assessed value |

| Annual city planning tax | Applies to property within designated urban planning zones. | Up to 0.3% of assessed value |

Most taxes are calculated from the property’s assessed value (固定資産評価額), not the purchase price, and the assessed value is usually well below market price, which keeps the actual tax bill lower than the headline rates suggest. The reduced 1.5% land registration rate runs through 31 March 2029, and reduced building registration rates through 31 March 2027, so check current rates with your agent before closing. The real estate acquisition tax bill arrives 3–6 months after registration, so set funds aside for it.

As the chart shows, the agent fee is the single largest line item in your closing costs, typically larger than all government taxes combined. This is why choosing the right agent matters: in Japan, your broker does the work that a lawyer would handle elsewhere, including contract drafting, legal disclosures, and title transfer coordination. The fee you pay is for that full scope of work, not just property search.

These percentages are a rough estimate based on a sample Tokyo residential purchase. Actual costs vary depending on the property’s assessed value, whether reduced tax rates apply, and the type of building. For a complete breakdown of every tax and fee involved in a Japanese property purchase, read our full guide to buying taxes and fees.

Other costs might include registration fee and or property management fees. There is also Asset Tax and City Tax that count as ongoing yearly costs of owning a property in Japan as well as loan/mortgage repayments if you have borrowed.

To get an estimate on your monthly loan payments in Japan, you can refer to our Yen Loan Calculator.

What Documents Do You Need to Buy a House in Japan?

The required documents depend on whether you live in Japan or abroad. In both cases, your agent and judicial scrivener will guide you through the exact paperwork.

If You Live in Japan

- Residence card and passport

- Inkan (registered personal seal) and seal certificate (印鑑登録証明書)

- Proof of income, three years of records if applying for a mortgage

If You Live Outside Japan

- Passport

- Notarised affidavit in place of the inkan and seal certificate

- Proof of address, often in the form of a utility bill or bank statement

- From April 2026: information needed for the FEFTA Form 22 filing, see below

What Changed for Foreign Buyers in 2026?

Two important administrative changes took effect in April 2026. Neither restricts your right to buy, both add a reporting step.

1. FEFTA Form 22 Reporting for Non-Residents

From 1 April 2026, all non-resident buyers acquiring real estate in Japan must file Form 22 with the Bank of Japan within 20 days of acquisition. The form covers property type, location, area, acquisition date, and price. A licensed real estate agent or judicial scrivener can submit it on your behalf, which is the standard approach. The filing is for government statistics and compliance; it does not block your purchase.

2. Nationality Disclosure at Registration

Under the Ministry of Justice’s amendment to the Real Property Registration Rules (不動産登記規則), published for public comment on 23 December 2025, every property buyer, Japanese and foreign, must declare their nationality when applying for ownership registration at the Legal Affairs Bureau. The amendment is scheduled to take effect in early fiscal year 2026. Nationality is recorded only in an internal “search information management file” maintained by the Ministry of Justice and does not appear on the public Real Property Register (登記簿). Privacy protections apply equally to all buyers.

What did NOT change: Foreign nationals still have the same property ownership rights as Japanese citizens. There is no foreign ownership cap, no minimum investment, no reciprocity test, and no “golden visa”, buying a house does not give you a visa or residency.

What Should Expats Know Before Buying a House in Japan?

A few features of the Japanese system regularly surprise international buyers. Understanding them up front avoids costly mistakes.

Lawyers Are Not Part of a Standard Purchase

Japan does not use a notary or buyer-side lawyer for residential property. Licensed brokers and judicial scriveners handle the legal work. This makes choosing an experienced, well-staffed agency far more important than in markets where a separate lawyer reviews everything.

All Documents Have Legal Effect Only in Japanese

Every contract, disclosure, and registration is in Japanese. Reputable agencies provide English translations, but only the Japanese version has legal standing, translations are reference materials. Always work with an agency that has both bilingual front-line staff and a Japanese-qualified legal team behind them.

Ownership is Confirmed by Registration, Not by Signing

In some countries, the moment you sign and pay you are the owner. In Japan, ownership only becomes legally secure when your name is recorded in the official property register at the Legal Affairs Bureau. Your judicial scrivener handles this within days of settlement, but it is the registration, not the contract, that secures your title.

Non-Resident Owners Need a Tax Representative

If you live outside Japan, you must appoint a tax representative (納税管理人, nōzei kanrishin) at a Japan address to receive your fixed asset tax bill each year. Many foreign buyers use their judicial scrivener, agent, or a specialised mail-handling service for this.

Should You Buy in Japan for Short-Term Rental Income?

Japan’s 2018 Private Lodging Business Act (民泊新法) caps short-term rentals at 180 days per calendar year, and around 99% of condominium management associations prohibit short-term rentals entirely in their bylaws. Tokyo wards including Shinjuku, Shibuya, and Minato restrict residential-zone minpaku further to weekends and holidays. That does not close the door on short-term rental income, it just means the property type and operating model matter more than they would elsewhere. Investors typically pursue one of three routes: buying an entire apartment building, developing in a designated National Strategic Special Zone (特区民泊) that allows 365-day operation, or operating under a hotel or ryokan licence (旅館業法) instead of minpaku.

Housing Japan’s sister company, Ken’s Place, specializes in this work across central Tokyo, Minami Azabu, Roppongi, Azabu-juban, Omotesando, and Akasaka, supporting investors through business planning, design, license application, and day-to-day operation. If short-term rental income is part of your buying thesis, talking to both teams early keeps the acquisition and the operating model aligned from day on.

How Does the Process Differ for Residents and Non-Residents?

Most legal points are identical. The differences are practical: which IDs you can use, which banks will lend to you, and which reports you must file.

| Item | Resident in Japan | Non-resident overseas buyer |

|---|---|---|

| Right to buy | Same as Japanese citizens | Same as Japanese citizens |

| ID required | Residence card, passport, inkan | Passport plus a notarized affidavit in place of an inkan |

| Mortgage access | Available from most major banks at competitive rates | Generally, cash-only; a small number of lenders work with non-residents |

| FEFTA reporting | Not required for personal home purchase | Form 22 to the Bank of Japan within 20 days of acquisition (from April 2026) |

| Tax representative | Not required | Required to receive property tax bills in Japan |

Why Buy a House in Tokyo?

Tokyo combines deep liquidity, strong rule of law, and globally low borrowing costs. Property rights are secure, the title system is transparent, and Tokyo is one of the world’s most connected business cities through exceptional public transport, bullet trains and Haneda and Narita airports. Rental yields in central Tokyo typically run 3–5% gross, with prime wards like Minato sitting at the lower end and emerging areas at the higher end (Housing Japan market analysis). Yields in the 23 wards as a whole average around 4%, while regional cities can reach higher levels in exchange for greater vacancy risk.

For owner-occupiers, the appeal is the city itself, efficient transport, world-class amenities, low crime, and architecture that ranges from quiet residential streets in Hiroo to landmark high-rises in Minato and Shibuya. For investors, the combination of yen-denominated assets and a stable legal framework make Tokyo a natural diversification market.

Ready to Buy a House in Tokyo?

Housing Japan has guided international buyers through the Tokyo property market for over 25 years. Our bilingual team is licensed by Tokyo Metropolitan Government and handles every step of the purchase, from off-market property sourcing and contract negotiation to FEFTA filings and tax representative services for non-residents.

Contact our expert bilingual Tokyo real estate agents:

Q&A: Buying a House in Japan as an Expat

Can foreigners buy property in Japan in 2026?

Yes. Foreign nationals can buy land, houses, and apartments in Japan in 2026 with the same legal rights as Japanese citizens. There are no nationality, residency, or visa requirements. From April 2026, non-residents must file a Bank of Japan FEFTA Form 22 within 20 days of acquisition, and all buyers disclose nationality at registration, but neither rule blocks foreign purchases.

Do I need a visa or residency to buy a house in Japan?

No. You do not need a Japanese visa or residence permit to buy property in Japan. Citizens of 71 countries, including the United States, United Kingdom, Australia, and most of the EU, can enter Japan visa-free for up to 90 days, which is enough time to view properties and sign a purchase contract. Buying a house does not grant you any visa or right to live in Japan long-term, those are handled separately by the Immigration Services Agency.

How much does it cost to buy a house in Japan?

Total buying costs in Japan typically run 5 to 6 percent of the purchase price, with an additional 1 to 2 percent in bank fees if you take a mortgage. The largest single cost is the brokerage fee, capped at 3% of the price plus ¥60,000 plus 10% consumption tax. Other costs include registration tax (1.5% on land, reduced rate extended through 31 March 2029), real estate acquisition tax (3% on residential land and homes), stamp duty, and judicial scrivener fees.

Can foreigners get a mortgage in Japan?

It depends on your residency status. Foreign nationals living in Japan with stable local income can get a mortgage from most major banks at the same rates as Japanese citizens. Non-resident buyers living overseas have far fewer options, most Japanese banks require Japan residency and Japan income, but a small number of specialist lenders offer mortgages to non-residents, usually at higher rates and with loan-to-value ratios of 50–70%.

How long does it take to buy a house in Japan?

A standard purchase in Japan takes 60 to 90 days from the initial Letter of Intent to final settlement and key handover. Cash buyers can sometimes close in 30 to 45 days. The main steps are property search and viewings, contract negotiation, deposit payment, mortgage approval (if applicable), and final settlement at the buyer’s bank. Title transfer registration at the Legal Affairs Bureau usually completes within a few business days of settlement.

What is FEFTA Form 22 and do I need to file it?

FEFTA Form 22 is the report non-resident buyers file with the Bank of Japan after acquiring real estate in Japan. From 1 April 2026, all non-residents must file it within 20 days of acquisition, regardless of whether the property is for residence or investment. Your real estate agent or judicial scrivener can file on your behalf, which is the standard practice. The filing is for government statistics and does not require approval to complete your purchase.

Are there areas in Japan where foreigners cannot buy property?

There are no general bans, but a small number of designated zones near defence facilities, government installations, and remote border islands fall under the Important Land Survey Act. Buyers in these zones must file a post-transaction notification within two weeks of signing. Central Tokyo, Osaka, Fukuoka, and other major urban markets are not affected. Your agent will check the zoning before you make an offer.

Do I have to pay tax in Japan if I rent out my property?

Yes. Rental income from Japanese real estate is taxable in Japan regardless of where the owner lives. Non-resident landlords are subject to a 20.42% withholding tax when the tenant is a Japanese company, paid directly to the tax office. Income tax is filed annually and tax treaties (such as the US-Japan and UK-Japan treaties) usually prevent double taxation. A licensed Japanese tax accountant should handle the filings.

Can I do Airbnb with a property I buy in Japan?

Often no. Japan’s minpaku law caps short-term rentals at 180 days per year, and around 99% of condominium management associations prohibit short-term rentals in their bylaws. Detached houses give you more flexibility, but municipal rules vary widely, Tokyo wards such as Shinjuku, Shibuya, and Minato restrict residential-zone minpaku to weekends and holidays. Always confirm building bylaws and ward rules in writing before buying for short-term rental income.

Why work with Housing Japan?

Housing Japan has been guiding international buyers through Tokyo property purchases for 25 years. Our bilingual agents are licensed by Tokyo Metropolitan Government, our staff handle the FEFTA filing and tax representative requirements directly, and we have a track record across both on-market and exclusive off-market luxury inventory in central Tokyo. Contact us for a confidential consultation about your purchase.

Written by Housing Japan’s editorial Team. Housing Japan is a licensed brokers with over 25 years of experience helping international buyers purchase homes in Tokyo.

Sources used for this blog:

Note: Note: Housing Japan is involved in property sales and development in Tokyo. We act in the buyer’s best interest and only recommend properties that align with your needs, circumstances, and goals. Information here is for general guidance and is not legal or tax advice. Always consult a licensed Japanese tax professional for personal advice.